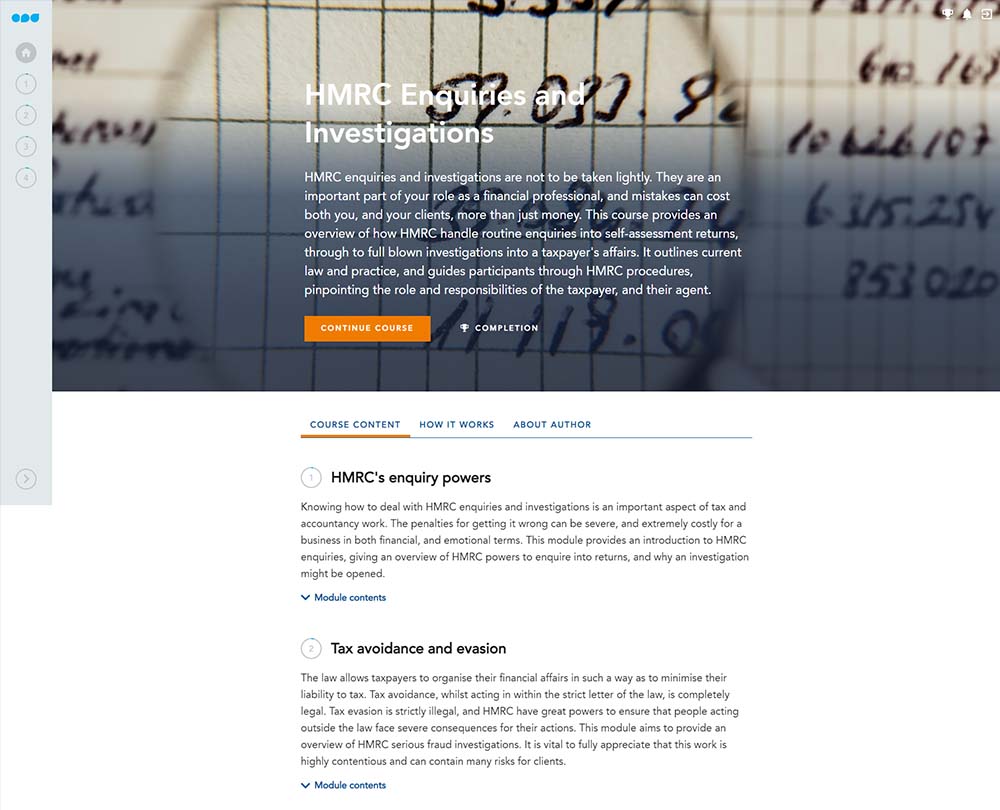

HMRC Enquiries and Investigations

Revised and up to date for 2025/26. Mistakes with HMRC enquiries and investigations can cost you more than just money. This course looks at how HMRC handle routine enquiries into self-assessment returns, through to full blown investigations into a taxpayer’s affairs.

£100 +VAT

HMRC Enquiries and Investigations

£100 +VAT

HMRC Enquiries and Investigations

This course is not currently available. To find out more, please get in touch.

This course will enable you to

- Deal with HMRC enquiries and investigations

- Understand HMRC’s powers, the different types of investigations and why an investigation might be opened

- Negotiate a settlement, and mitigate penalty charges

- Be clear about the difference between tax avoidance and evasion

- Understand why HMRC might start a criminal investigation, and the powers and safeguards under which they must operate

About the course

HMRC enquiries and investigations are not to be taken lightly. They are an important part of your role as a finance professional, and mistakes can cost both you, your company or your clients, more than just money.

This course looks at how HMRC handle routine enquiries into self-assessment returns, through to full blown investigations into a taxpayer’s affairs. It outlines current law and practice, and guides participants through HMRC procedures, pinpointing the role and responsibilities of the taxpayer, and their agent.

Please Note: This course is only relevant to the UK

Contents

HMRC’s enquiry powers

The types of enquiry

The importance of HMRC’s enquiry powers

Under further examination

Opening an enquiry

The time frame for opening an enquiry

Cause for concern

Reducing the risk

Tax avoidance and evasion

The difference between evasion and avoidance

Tax evasion: explained

The general anti-abuse rule

Dealing with tax fraud and criminal investigations

The Contractual Disclosure Facility

Practical aspects

How to handle an enquiry

During an enquiry

Calculating penalties

Negotiating a settlement

Alternative Disclosure Resolution (ADR)

Criminal investigations

How to handle a criminal investigation

Instigating criminal proceedings

HMRC’s investigation powers

Using HMRC’s criminal powers

Time limits for complaints

How it works

Author

Sarah Laing

Sarah is a Chartered Tax Accountant (CTA) and a member of the Chartered Institute of Taxation (CIOT). Sarah currently works as a freelance tax author providing technical writing services to the tax and accountancy professions.

You might also like

Take a look at some of our bestselling courses