IFRS: Sector Specific Standards

This course covers four IFRSs that are specific to particular sectors: agriculture, exploration and evaluation of mineral reserves, insurance, and regulatory deferral accounts, for first time adopters of IFRS in sectors subject to price or rate regulation.

£100 +VAT

IFRS: Sector Specific Standards

£100 +VAT

IFRS: Sector Specific Standards

This course is not currently available. To find out more, please get in touch.

This course will enable you to

- Understand the strange and unique provisions of IAS 41 Agriculture, including the recognition and measurement of biological assets

- Account for the massive cost and potential benefits of exploration and evaluation of mineral resources under IFRS 6

- Discover why IFRS 17 Insurance Contracts came into existence and its application to financial statements

- Learn about IFRS 14 Regulatory Deferral Accounts and its application

About the course

Some of the most interesting and curious of the IFRS standards concern specific sectors. Understanding them not only ensures we know about the special provisions, but also shines a light on our practices elsewhere.

IAS 41 deals with agriculture, the only sector where new assets are literally born! IFRS 6 deals with an issue specifically excluded by several other standards – the exploration and exploitation of mineral resources. The new standard, IFRS 17 Insurance Contracts, has clarified a particularly tricky area, and IFRS 14 Regulatory Deferral Accounts is critical for first time adopters of IFRS who are subject to rate regulation, such as the public utilities. Discover more about these specific standards, their objectives and disclosure requirements.

Contents

Agriculture

IAS 41 Overview

Objectives and scope

Key definitions

Recognising and measuring biological assets

IAS 41 Q&A

Reliable measurement and government grants

Disclosures

Additional disclosures

Mineral resources

IFRS 6 Overview

Objective and scope

Measurement and recognition

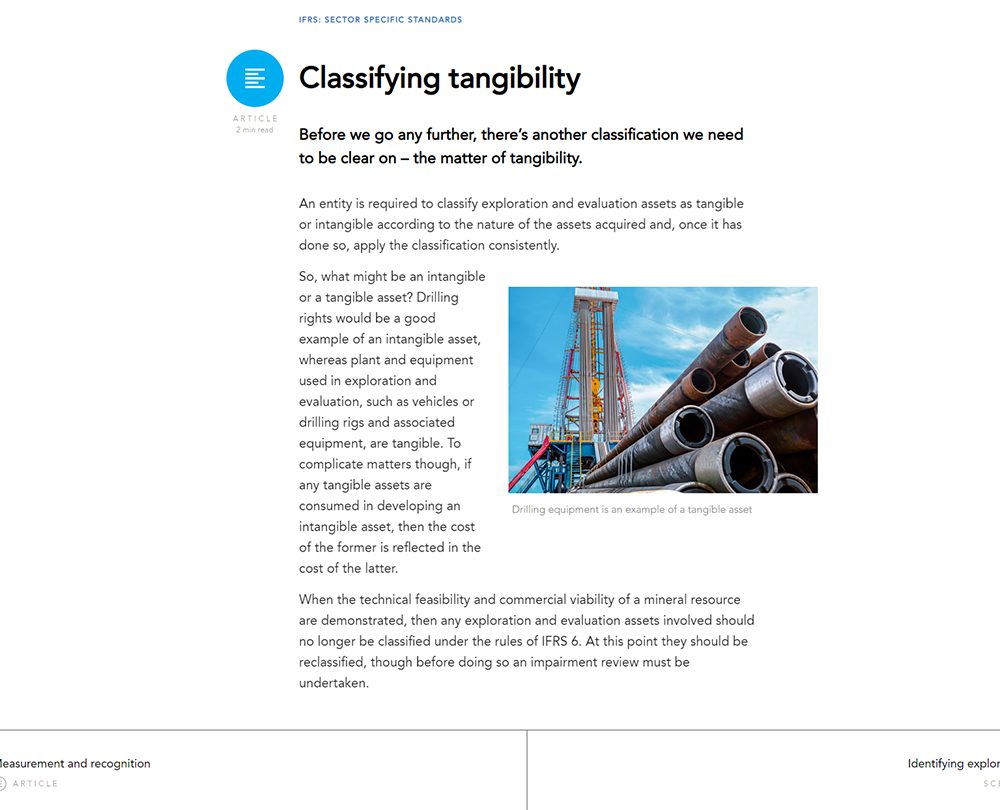

Classifying tangibility

Impairment

Disclosures

Insurance contracts

IFRS 17 Overview

A complicated history

A significant step forward

Recognition and measurement

Modification, derecognition and presentation

Disclosures

Regulatory deferral accounts

IFRS 14 Overview

Objective and scope

Key definitions

IFRS 14 and GAAP

Presentation

Disclosures

How it works

Author

Wayne Bartlett

Wayne is an internationally acclaimed speaker and trainer on all aspects of public and private sector accounting and auditing standards. He has been instrumental in helping to develop the profession internationally and has taken lead roles in the development of new professional bodies and the accounting profession in Mozambique and Rwanda, and been extensively involved in developing financial reporting in many countries across the globe.

You might also like

Take a look at some of our bestselling courses